Precision Trade Simulation for Developers

Refine and validate your trading strategies using accurate historic market data. algostress generates detailed CSV outputs tailored for algorithmic research.

Reliable Simulation Meets Algorithmic Performance

Synthetic market stress-data generator for algo trading bot developers.

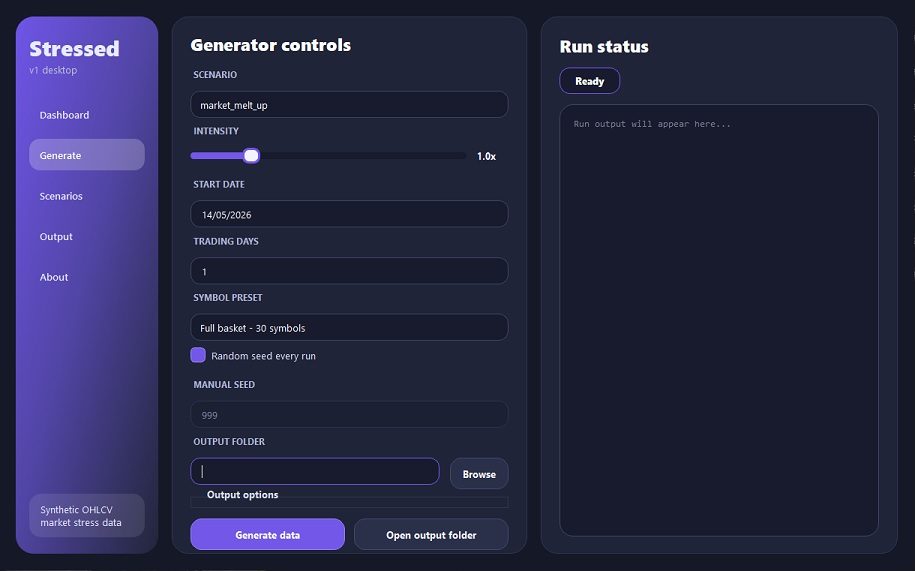

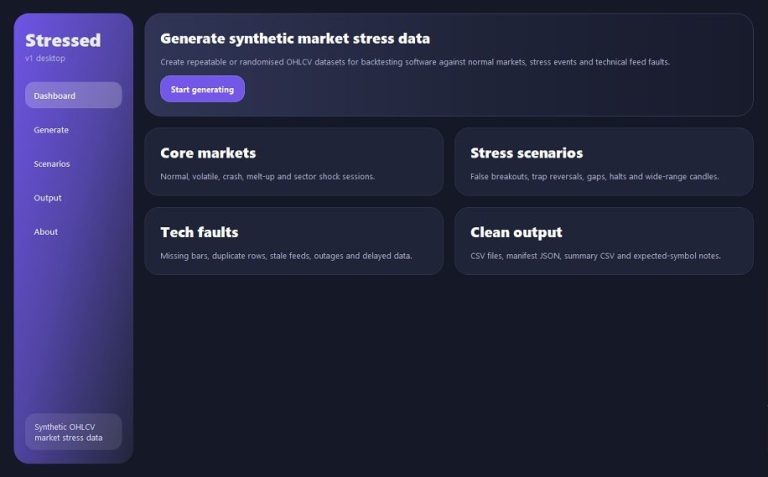

Stressed v1 is a desktop tool that creates realistic synthetic 1-minute OHLCV market data for testing trading bots, backtesters, risk controls, and execution logic. Instead of relying only on clean historical data, it lets developers generate controlled market conditions such as crashes, melt-ups, volatility bursts, bear traps, bull traps, spread shocks, bad ticks, missing data, stale feeds, duplicate rows, and exchange-style outages.

It is not designed to predict markets. It is designed to break weak assumptions before real money or live systems do.

Key Features for Algorithmic Trading Success

Stress-test your trading bot before the market does.

Accurate Market Simulation

Stressed v1 is a synthetic market stress simulator for algo trading developers.

CSV Output for Backtesting

It generates configurable 1-minute OHLCV data designed to test how trading bots behave under difficult market and data-feed conditions.

Developer-Friendly Interface

Create market crashes, melt-ups, bull traps, bear traps, volatility bursts, bad ticks, missing candles, stale feeds, duplicate rows, and exchange-style outages, then export the results as simple CSV files for backtesting.

Robust Performance

Stressed v1 helps developers find fragile logic, unsafe assumptions, and weak risk controls before deploying bots into live or paper trading environments.

Feedback

Email : jason@algostress.com